Defining KYC Zero in 2026

The term "KYC Zero" is often misunderstood as a method to bypass legal obligations. In reality, it represents a shift from data collection to data verification. Instead of storing sensitive personal information, systems use zero-knowledge proofs (ZKPs) to confirm that a user meets specific compliance criteria without revealing the underlying data.

This approach minimizes data exposure while satisfying Anti-Money Laundering (AML) standards. For example, a platform can verify that a user is over 18 or resides in a permitted jurisdiction using a cryptographic proof. The verifier accepts the proof as valid without ever seeing the birthdate or address. This reduces the risk of data breaches and limits the attack surface for malicious actors.

In 2026, true KYC Zero is rare on regulated fiat gateways. Most services still require some level of identification for fiat on-ramps. However, the trend is moving toward "low-KYC" models where verification steps are lighter and less intrusive. This allows for faster transactions while maintaining a baseline of regulatory compliance.

The core benefit is that compliance becomes a technical check rather than a data storage exercise. By proving predicates like age or residency, users retain control over their personal information. This aligns with evolving privacy regulations that emphasize data minimization and purpose limitation.

How zero-knowledge proofs work

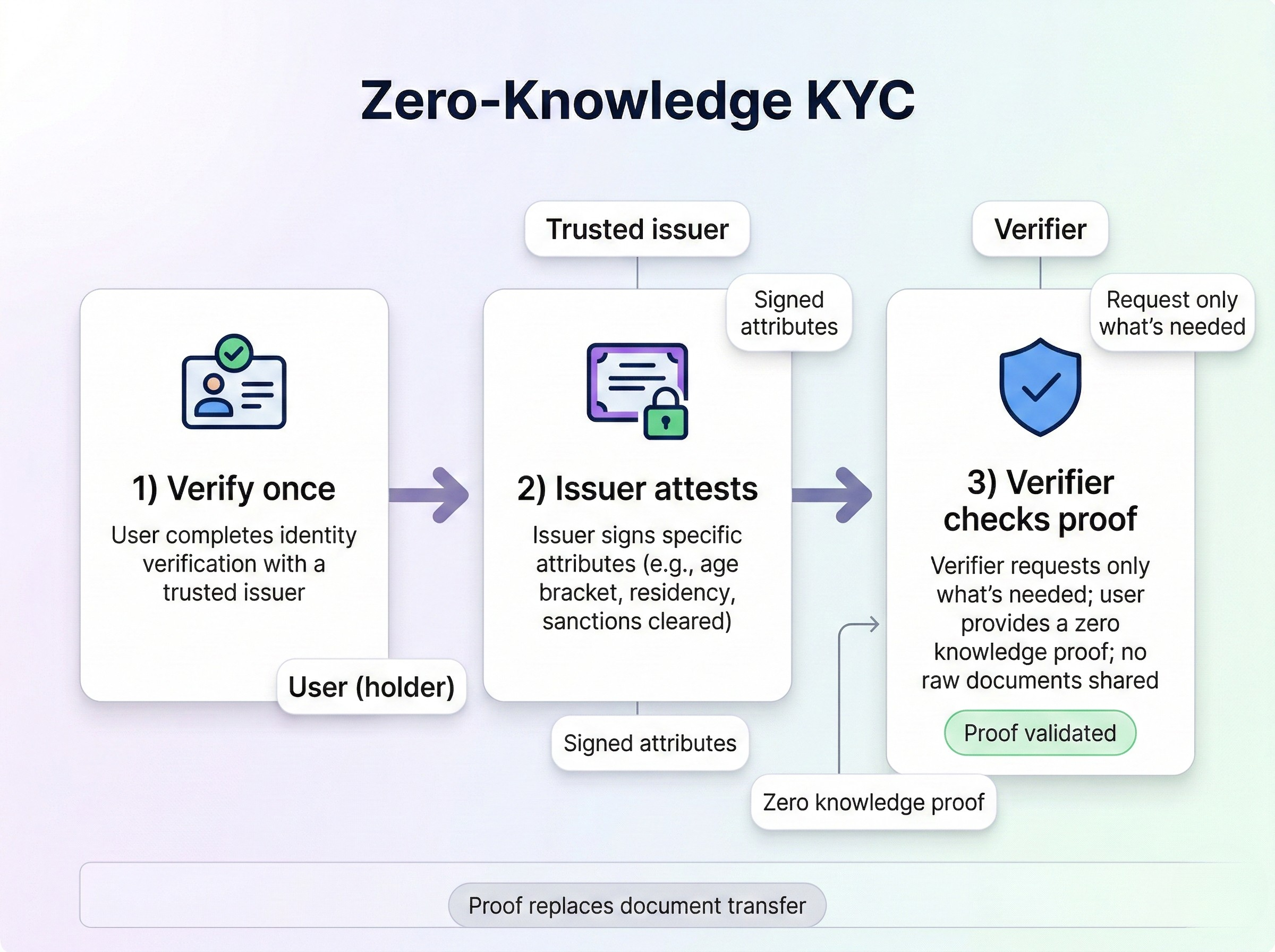

Zero-knowledge proofs (ZKPs) function as a cryptographic protocol that allows one party to prove a statement is true without revealing any information beyond the validity of the statement itself. In the context of KYC compliance, this mechanism enables a user to demonstrate that they meet specific regulatory criteria without disclosing the underlying personal data to the verifier. This approach fundamentally shifts the data model from centralized storage of sensitive identity documents to decentralized verification of compliance predicates.

The process involves two distinct roles: the prover, who holds the private data, and the verifier, who needs to confirm a specific claim. Consider a scenario where a financial institution must verify that a customer is over the age of 18 and resides in the European Union. Instead of uploading a passport or driver’s license, the user’s application generates a cryptographic proof. This proof confirms that the birth date on the document is before a certain cutoff and that the address matches an EU registry, without exposing the actual date, name, or document number.

The user inputs their private credentials (e.g., date of birth, residency status) into a trusted setup or local application. This data remains on the user’s device and is never transmitted in plaintext.

The application compiles the verification logic into a mathematical circuit—a set of constraints that define what constitutes a valid proof. For example, the circuit enforces that the year of birth is less than the current year minus 18.

Using the private data and the circuit, the prover generates a succinct cryptographic proof. This proof is a small string of data that mathematically guarantees the constraints were satisfied without revealing the input values.

The verifier receives the proof and runs it against the public verification key. If the proof is valid, the verifier accepts the claim (e.g., "User is 18+ and EU-resident") with cryptographic certainty, having learned nothing else about the user’s identity.

This architecture ensures that compliance requirements are met without creating a honeypot of sensitive personal information. Regulators can audit the verification logic and the proofs themselves, while users retain control over their data. The system relies on the mathematical certainty of the proof rather than the trustworthiness of a central database holding identity records.

Self-Sovereign Identity Architecture

In a KYC Zero framework, the traditional model of centralized data storage is replaced by a decentralized architecture where users hold their own credentials. Instead of submitting copies of passports or utility bills to a bank’s server, users store verified identity attributes in a personal digital wallet. This shift establishes self-sovereign identity (SSI), granting individuals direct control over their personal data and how it is shared.

The core mechanism enabling this control is the zero-knowledge proof (ZKP). A ZKP is a cryptographic method that allows a prover to convince a verifier that a statement is true without revealing the underlying data itself. In practical compliance terms, this means a user can prove they are over 18 or a resident of a specific jurisdiction without disclosing their exact birthdate or home address. The verifier receives only a cryptographic confirmation that the predicate is met, not the raw personal information.

This selective disclosure model significantly reduces the attack surface for data breaches. Since financial institutions no longer store large repositories of sensitive identity documents, the incentive for hackers to target these entities diminishes. The architecture ensures that data remains with the user, who can grant or revoke access to specific attributes on a per-transaction basis.

Traditional KYC vs. KYC Zero Architecture

The table below contrasts the operational differences between legacy compliance models and the emerging self-sovereign standard.

| Feature | Traditional KYC | KYC Zero (SSI) |

|---|---|---|

| Data Storage | Centralized databases | User-held digital wallets |

| Data Exposure | Full document upload | Selective attribute disclosure |

| User Control | Limited; institution-owned | Full; user-managed |

| Breach Risk | High; single point of failure | Low; decentralized attributes |

Regulatory Alignment and AML Standards

Zero-Knowledge Proof KYC (ZK-KYC) is designed to reconcile the conflicting demands of strict financial compliance and user data privacy. By utilizing cryptographic proofs, users can demonstrate adherence to regulatory criteria without exposing the underlying personal data. This approach satisfies the core requirement of Anti-Money Laundering (AML) frameworks: verifying that an individual meets specific legal thresholds while keeping their identity records secure.

The Financial Action Task Force (FATF) guidelines emphasize the need for accurate customer identification and risk assessment. ZK-KYC aligns with these standards by allowing institutions to verify predicates such as age, residency, or sanction list status. For example, a user can prove they are over 18 or reside in a permitted jurisdiction without revealing their exact birth date or home address. This selective disclosure ensures that institutions collect only the data necessary for compliance, reducing the risk of data breaches and unauthorized profiling.

In the European Union, eIDAS 2.0 introduces the European Digital Identity Wallet, which sets new benchmarks for digital trust and privacy. ZK-KYC integrates naturally with this framework by enabling interoperable verification across borders. Users can present verifiable credentials from their digital wallets to financial institutions, proving their eligibility for services without transferring sensitive documents. This mechanism supports the EU’s goal of enhancing digital sovereignty while maintaining robust AML controls through cryptographically secure, privacy-preserving verification methods.

Adoption Challenges and Market Reality

The transition to KYC Zero is not merely a technical upgrade but a structural overhaul of compliance infrastructure. While the promise of zero-knowledge proofs (ZKPs) offers undeniable privacy benefits, the friction in adoption stems from three primary areas: computational overhead, the lack of unified standards, and the critical distinction between true privacy and unregulated anonymity.

First, the computational cost of generating and verifying ZK proofs remains a barrier for high-throughput financial systems. Unlike traditional database queries, ZKPs require significant processing power to create succinct arguments that verify specific predicates—such as confirming a user is over 18 or resides in a permitted jurisdiction—without revealing the underlying identity. For institutions, this translates to higher operational costs and latency that legacy systems do not impose.

Second, the market suffers from a standardization gap. There is currently no universal protocol for how different jurisdictions interpret and accept ZK-based credentials. A proof valid under the EU’s MiCA framework may not align with compliance requirements in other regions, forcing platforms to maintain complex, fragmented verification stacks. This fragmentation increases the risk of regulatory missteps and complicates cross-border interoperability.

Finally, it is essential to distinguish KYC Zero from "no-KYC" services. As noted by Guardarian, in 2026, no-KYC crypto rarely means zero checks on a regulated fiat gateway; it usually implies a lighter checkout process with fewer intrusive steps. True KYC Zero, however, involves rigorous cryptographic verification of eligibility without exposing personal data. Confusing these two models creates regulatory ambiguity, as authorities may view "lighter" checks as insufficient anti-money laundering (AML) safeguards. Robust infrastructure and clear regulatory frameworks are required to replace legacy systems effectively.

No comments yet. Be the first to share your thoughts!