Define the KYC Zero 2026 workflow

KYC Zero 2026 is not about removing compliance; it is about automating it so the user never sees the friction. The goal is to shift from manual, high-friction checks to automated, invisible verification that meets new regulatory deadlines. This means building a system where identity confirmation happens in the background, allowing the customer to proceed without interruption.

The workflow begins with the user initiating an account. Instead of asking for documents immediately, the system first attempts to verify identity through passive data sources or existing trusted credentials. If the system cannot automatically confirm the user’s identity, it then requests specific evidence, such as a government ID or selfie, only for the fields that failed initial checks. This minimizes the burden on the user and reduces the volume of manual reviews required by compliance teams.

By 2026, regulatory frameworks like the EUDI Wallet requirements will mandate that banks and financial institutions accept digital identity credentials from authorized providers. This shift allows for real-time, cryptographically verified identity checks that are far more accurate than traditional document uploads. The workflow must be designed to integrate these new standards seamlessly, ensuring that the verification process is both secure and compliant with evolving laws.

The final step in the workflow is continuous monitoring. Once a user is onboarded, the system must periodically re-verify their identity based on their risk category. High-risk customers may require re-verification every two years, while low-risk customers might only need it every ten years. This dynamic approach ensures that compliance is maintained without imposing unnecessary friction on every user interaction.

Set up automated identity verification

Manual document review creates bottlenecks that frustrate users and delay revenue. Automated identity verification replaces this friction by using optical character recognition (OCR) and liveness detection to validate credentials in real time. This shift from human-in-the-loop processing to algorithmic decision-making is the foundation of frictionless onboarding.

The following steps outline the technical implementation of an automated KYC pipeline. Each stage must be configured to handle specific data inputs and validation logic before passing the result to your compliance team.

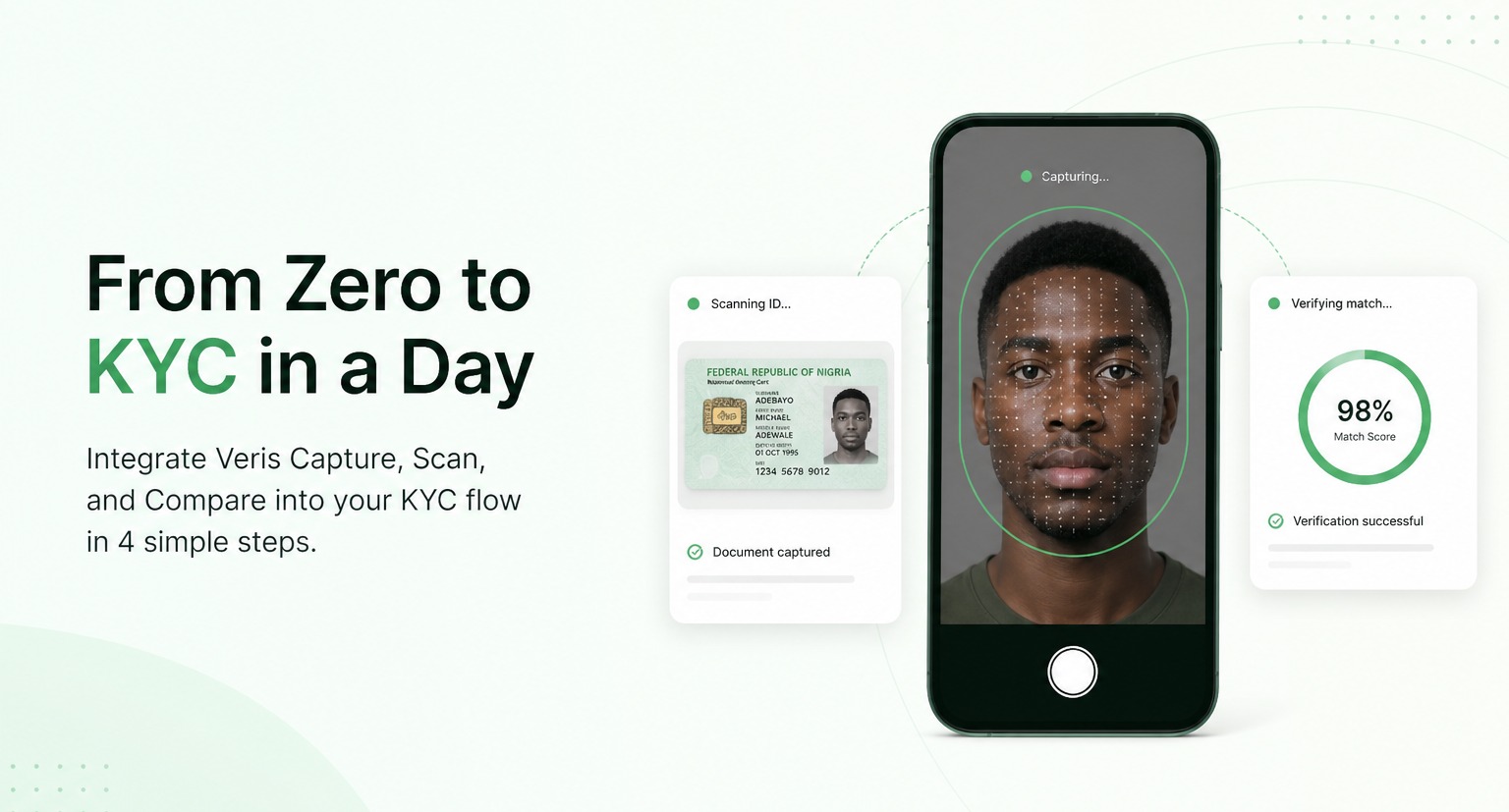

Begin by integrating an SDK or API that captures government-issued IDs via the user’s mobile device. The system must extract text fields (name, date of birth, document number) and verify the document’s structural integrity. Look for signs of tampering, such as altered fonts or mismatched holograms. This initial pass ensures the data is machine-readable before moving to biometric checks.

To prevent spoofing attacks using photos or deepfakes, require a liveness check. This step captures a short video or series of images to confirm the user is a live person present at the time of verification. Modern systems use passive liveness detection, which analyzes micro-movements and screen reflections without requiring the user to perform specific actions, keeping the experience seamless.

Cross-reference the extracted identity data against global sanctions lists, politically exposed persons (PEP) databases, and adverse media sources. This step verifies that the user is not on any regulatory blacklist. Configure confidence thresholds to automatically approve clear matches and flag borderline cases for manual review, ensuring compliance with anti-money laundering (AML) regulations.

KYC is not a one-time event. Set up a backend service that periodically re-verifies user identities and monitors for changes in risk status. This continuous trust model ensures that your platform remains compliant as regulations evolve and new threats emerge. Automated alerts notify your compliance team if a user’s status changes, allowing for proactive risk management.

Implementing this automated flow reduces onboarding time from days to seconds. By relying on verified data sources and algorithmic validation, you minimize human error and ensure consistent compliance across all users.

Move to continuous trust monitoring

One-time identity verification is no longer sufficient. Customer risk profiles shift rapidly, often outpacing traditional periodic review cycles. To maintain compliance in 2026, you must transition from static checks to perpetual KYC (pKYC). This approach treats identity verification as a continuous, event-driven process rather than a one-off gate.

Implementing pKYC requires integrating real-time data streams that trigger alerts when specific risk indicators change. Instead of waiting for a scheduled review, your system should automatically reassess a customer’s status the moment new information becomes available.

1. Define Real-Time Risk Triggers

Identify the specific events that require immediate re-verification. Common triggers include adverse media mentions, sanctions list updates, or sudden changes in transaction volume. Configure your compliance engine to listen for these signals continuously, ensuring that high-risk changes are flagged the moment they occur rather than months later.

2. Automate Data Refresh Cycles

Replace manual data collection with automated integrations to global watchlists and credit bureaus. Ensure your system pulls fresh data at intervals appropriate for the customer’s risk tier. High-risk customers may require daily checks, while low-risk profiles might only need weekly updates. This automation reduces operational drag while maintaining regulatory rigor.

3. Implement Dynamic Risk Scoring

Move beyond static risk ratings. Develop a dynamic scoring model that adjusts in real-time based on the latest data. If a customer’s score crosses a predefined threshold, the system should automatically restrict certain actions or prompt for additional verification. This creates a frictionless experience for low-risk users while adding necessary checks for those showing signs of elevated risk.

This shift from periodic to perpetual monitoring is becoming the industry standard. As noted in the 2026 KYC/AML Outlook, speed is now the deciding factor in compliance, with customer risk shifting faster than traditional review cycles can handle.

Audit your compliance automation stack

With the 2026 regulatory landscape tightening, your automated verification pipeline must do more than just scan documents. The Federal Register’s proposed enhancements to KYC requirements emphasize that accuracy is no longer optional; systems must actively confirm the validity of customer-provided information rather than passively collecting it.

Use this checklist to ensure your automation engine meets these stricter standards before deployment.

- EUDI Wallet readiness: Verify that your system can parse and validate European Digital Identity Wallet credentials, ensuring interoperability with upcoming EU standards.

- AI fraud detection: Audit your machine learning models for bias and accuracy. Ensure they can detect deepfakes and synthetic identities with high precision, as manual overrides are no longer sufficient for high-risk transactions.

- Data privacy compliance: Confirm that all data handling processes align with GDPR and local privacy laws. Ensure data minimization principles are baked into the automation logic, not just the UI.

- Periodic re-KYC cadence: Implement automated triggers for re-verification. High-risk customers require updates every two years, while medium-risk customers need checks every eight years.

- Travel Rule integration: Ensure your system can seamlessly exchange necessary originator and beneficiary information for virtual asset transfers, complying with FATF guidelines.

The goal is frictionless onboarding that doesn't sacrifice security. By automating these compliance checks, you reduce manual review times while maintaining the rigorous standards required by 2026 regulators.

Kyc 2026: common: what to check next

As the 2026 regulatory landscape shifts, businesses face updated compliance deadlines and new verification standards. Below are the most frequent questions regarding the periodic KYC cadence and the evolving legal definitions of customer due diligence.

These changes reflect a move toward frictionless yet secure onboarding. Staying ahead of the June 2026 deadline ensures your business remains compliant without sacrificing user experience.

No comments yet. Be the first to share your thoughts!