The 2026 Compliance Shift Toward Biometrics

The rise biometric identity verification in 2026 signals a fundamental structural change in how organizations prove customer identity. By this year, biometric KYC has moved from an optional convenience to a regulatory baseline. This shift is not merely technological; it is a response to the escalating sophistication of digital fraud and the regulatory imperative for stronger customer due diligence.

For years, Know Your Customer (KYC) protocols relied heavily on static documents and password-based authentication. These methods are increasingly vulnerable to synthetic identity fraud and credential stuffing. In contrast, biometric verification ties identity to immutable biological traits, creating a dynamic layer of security that static passwords cannot match. As noted by industry analysts, the current phase of biometric deployment is defined by smarter technology and strategic integration into compliance workflows.

Regulatory bodies in major jurisdictions are now explicitly encouraging or mandating stronger authentication methods. The focus has shifted from simple identity confirmation to continuous, behavior-aware verification. This transition aligns with broader anti-money laundering (AML) directives that require institutions to have a higher degree of confidence in the identities of their clients. The result is a compliance environment where biometric data serves as the primary anchor for trust.

This evolution also addresses the friction inherent in traditional onboarding. Users no longer need to manually upload documents or wait for manual review cycles. Instead, facial recognition and liveness detection provide instant verification. This seamless experience reduces drop-off rates while simultaneously satisfying the heightened scrutiny of compliance officers. The 2026 standard is thus a dual-purpose solution: it secures the institution against fraud while streamlining the user journey.

How biometric verification replaces passwords

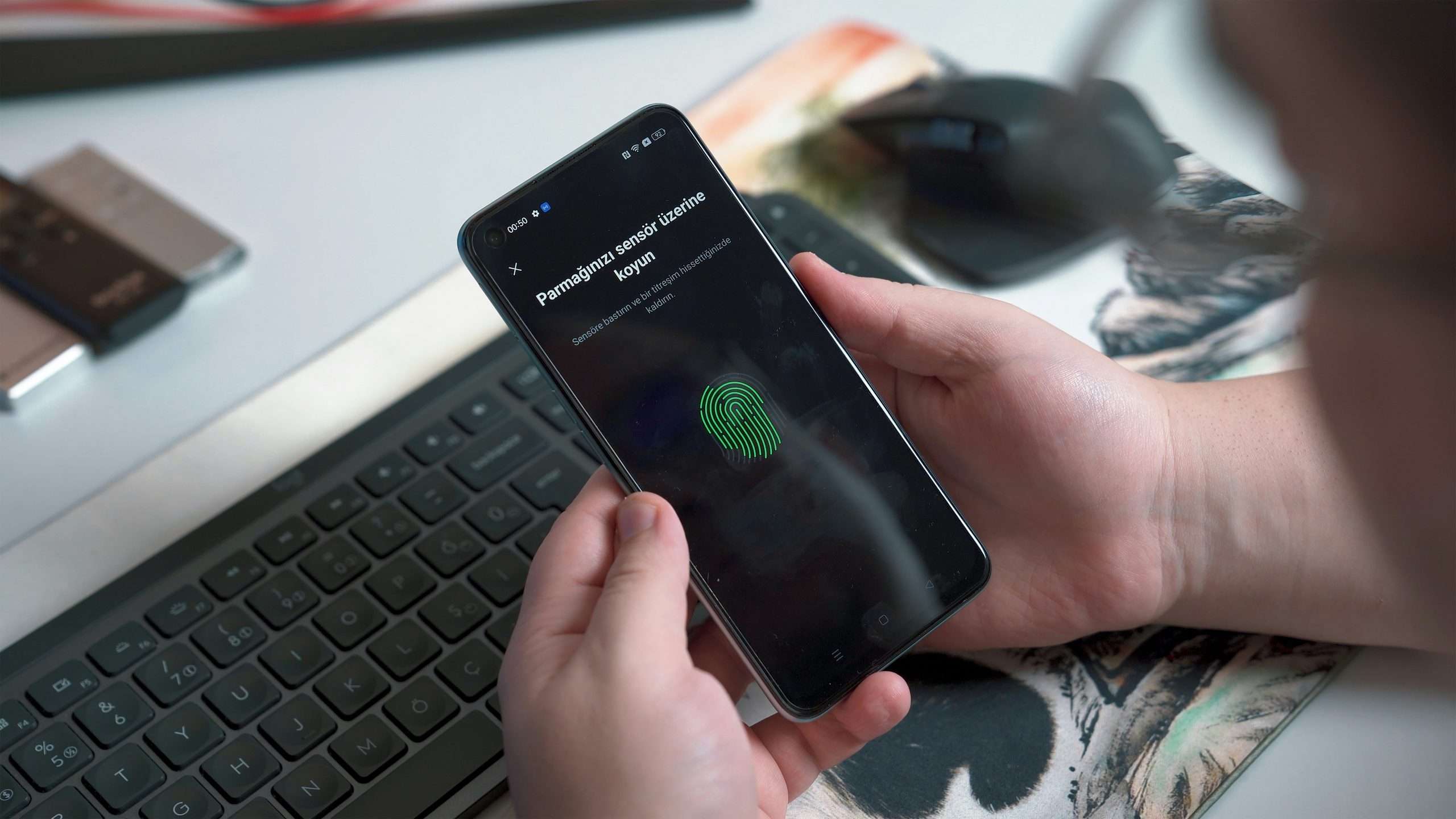

The shift toward passwordless verification in 2026 relies on biometric KYC to eliminate the single point of failure inherent in traditional authentication: the password. Instead of relying on memorized strings that can be phished or guessed, biometric systems create a unique digital signature based on physical traits like facial geometry or iris patterns. This fundamental change makes it significantly harder for fraudsters to impersonate users, as these traits are difficult to replicate compared to stolen credentials.

Two technical pillars support this transition: liveness detection and zero-knowledge proofs. Liveness detection ensures that the biometric sample is captured from a live person present at the device, rather than a static photo or deepfake video. This active verification step is critical for preventing replay attacks, where attackers attempt to reuse previously captured biometric data. Without liveness checks, even sophisticated biometric systems remain vulnerable to spoofing.

Zero-knowledge proofs (ZKPs) address the privacy and security concerns associated with storing sensitive biometric data. Rather than transmitting or storing the actual biometric template, ZKPs allow the system to verify that a user possesses a valid credential without revealing the underlying data. This cryptographic approach means that even if a database is breached, attackers cannot reconstruct the biometric traits or use them for identity theft elsewhere. The result is a system where the biometric data itself becomes irrelevant to the authentication process, rendering traditional password theft methods ineffective.

The combination of these technologies creates a robust framework for identity verification. As noted in recent industry analysis, biometric authentication and verifiable digital credentials provide the cryptographic foundation necessary for fraud prevention and regulatory compliance. This approach not only enhances security but also streamlines the user experience by removing the friction of password management. The focus shifts from remembering secrets to proving identity through inherent, unforgeable traits.

| Feature | Traditional Password KYC | Biometric KYC 2026 |

|---|---|---|

| Security Basis | Memorized secret string | Unique physical/biological trait |

| Phishing Resistance | Low (credentials can be stolen) | High (traits cannot be phished) |

| Spoofing Risk | N/A | Mitigated by liveness detection |

| Data Storage | Hashed passwords (vulnerable to rainbow tables) | Zero-knowledge proofs (data never exposed) |

| User Friction | High (memory, reset cycles) | Low (instant, passive verification) |

Data reflects industry trends in authentication security as of 2026.

Regulatory acceptance of digital identity

Global regulators are moving from cautious observation to formal acceptance of decentralized and biometric identity solutions. This shift reduces the legal ambiguity that previously surrounded passwordless systems, providing a clearer path for compliance in 2026. The focus is no longer on whether biometric data can be used, but on how it is governed under existing frameworks.

The European Union’s eIDAS 2.0 regulation, which came into effect in October 2024, establishes the legal foundation for European Digital Identity wallets. These wallets integrate biometric verification as a standard method for proving identity across borders. By recognizing eID schemes from member states, the regulation effectively legitimizes biometric checks as a compliant alternative to traditional document-based KYC. This creates a unified standard for financial institutions and service providers operating within the EU.

In the United States, the Financial Crimes Enforcement Network (FinCEN) has updated its guidance to acknowledge digital identity providers. While the USA PATRIOT Act remains the core statute, recent industry consultations signal a willingness to accept biometric data as a valid "identity verification" method when paired with appropriate safeguards. This regulatory flexibility allows banks to adopt passwordless onboarding without waiting for new federal legislation, provided they maintain robust audit trails.

Asia-Pacific jurisdictions are also accelerating adoption. Singapore’s Monetary Authority has issued clear guidelines supporting the use of biometric data in digital onboarding, provided that consent is explicit and data is stored securely. Similarly, the UK’s Financial Conduct Authority has updated its guidance to recognize non-traditional identity verification methods, including facial recognition, as compliant with anti-money laundering rules. These moves collectively reduce the legal risk for firms implementing biometric KYC 2026 strategies.

Reducing Identity Fraud and Account Takeover

Biometric KYC 2026 shifts the security paradigm from something you know to something you are. By replacing static passwords with unique biological traits, organizations significantly raise the barrier for identity fraud and account takeover attempts. Unlike passwords, which can be phished, guessed, or reused across platforms, biometric data is inherently tied to the individual. This makes it exponentially harder for malicious actors to impersonate legitimate users without the person’s physical presence.

The effectiveness of this approach is reflected in the rapid market expansion. The global biometric KYC market, valued at USD 27.8 billion in 2025, is projected to reach USD 104.2 billion by 2034 [src-serp-6]. This growth is not merely speculative; it is driven by financial institutions and regulated entities seeking robust defenses against rising cyber threats. As fraud techniques evolve, biometric verification provides a dynamic layer of security that adapts to the user’s unique physiological characteristics.

Implementing biometric KYC also reduces the administrative burden associated with fraud investigation. Traditional methods often require extensive manual review of suspicious activities, leading to delays and potential financial losses. With biometric data, the initial verification step is highly accurate, filtering out most fraudulent attempts before they reach human reviewers. This efficiency allows compliance teams to focus on genuine anomalies rather than routine false positives.

Implementation checklist for 2026

Transitioning to biometric KYC 2026 standards requires aligning technical infrastructure with evolving regulatory expectations. Compliance officers should audit current systems against the following priorities to ensure readiness for passwordless verification.

Review legacy databases for PII density. Ensure current records support the integration of liveness detection and facial recognition without requiring full customer re-onboarding.

Evaluate vendors against 2026 privacy frameworks. Prioritize providers offering on-device processing to minimize data residency risks and meet strict GDPR or local biometric law requirements.

Biometric KYC 2026 standards vary by region. Document specific consent and data retention rules for each operating jurisdiction to avoid cross-border compliance gaps.

Replace traditional passwords with biometric authentication in user journeys. Test the user experience to ensure conversion rates do not drop due to friction or privacy concerns.

Implement real-time anomaly detection for identity verification. Regularly update anti-spoofing models to counter deepfake attacks and emerging presentation attacks.

This phased approach ensures that biometric KYC 2026 implementations remain secure, compliant, and user-centric.

Common questions about biometric KYC 2026

Biometric KYC 2026 marks a shift toward passwordless verification, but adoption varies by region and industry. Below are answers to frequent questions about requirements, technology types, and future trends.

No comments yet. Be the first to share your thoughts!