Define the verification predicates

Zero-knowledge KYC 2026 begins by identifying exactly which regulatory facts must be proven without revealing the underlying data. Instead of collecting and storing sensitive personal information like full passports or biometric data, you establish specific claims about a user. This shift from "collect and store" to "prove what's needed" is the foundation of privacy-preserving compliance.

Start by listing the minimum necessary data points required for your specific regulatory environment. If your compliance framework only requires proof that a user is over 18, do not request their birthdate or full ID document. This approach limits the attack surface and reduces liability by ensuring you never hold more data than strictly necessary.

Next, map these data points to verifiable predicates. A predicate is a logical condition that can be proven mathematically. For example, rather than proving "I was born on [Date]," you prove "Age > 18." This ensures that the verifier receives only the confirmation of compliance, leaving the raw identity data private.

Select a trusted verification authority

Before you can issue a zero-knowledge proof, you need a trusted verification authority. In zero-knowledge KYC 2026, this entity performs the heavy lifting of initial identity checks. They confirm your identity against official documents and then issue a cryptographic credential. This credential proves you are verified without exposing your underlying data.

Think of the verification authority as a notary public for the digital age. You do not give your passport to every bank or exchange. Instead, you get your identity certified once by a trusted source. That certification is then packaged into a zero-knowledge proof. Any service can verify the proof without ever seeing your actual passport or address.

Choosing the right authority is critical. The provider must be recognized by regulators and compatible with your target platforms. Look for issuers that support standard protocols like W3C Decentralized Identifiers. This ensures your credential works across different ecosystems without needing constant re-verification.

Many financial institutions now partner with specialized identity providers. These providers handle the compliance burden while maintaining user privacy. By selecting a reputable issuer, you streamline the onboarding process. You avoid the friction of repeated document uploads and manual reviews.

Note: Ensure the verification authority you choose is compliant with local regulations. Using an unrecognized issuer may result in your credentials being rejected by regulated platforms.

Configure the zero-knowledge circuit

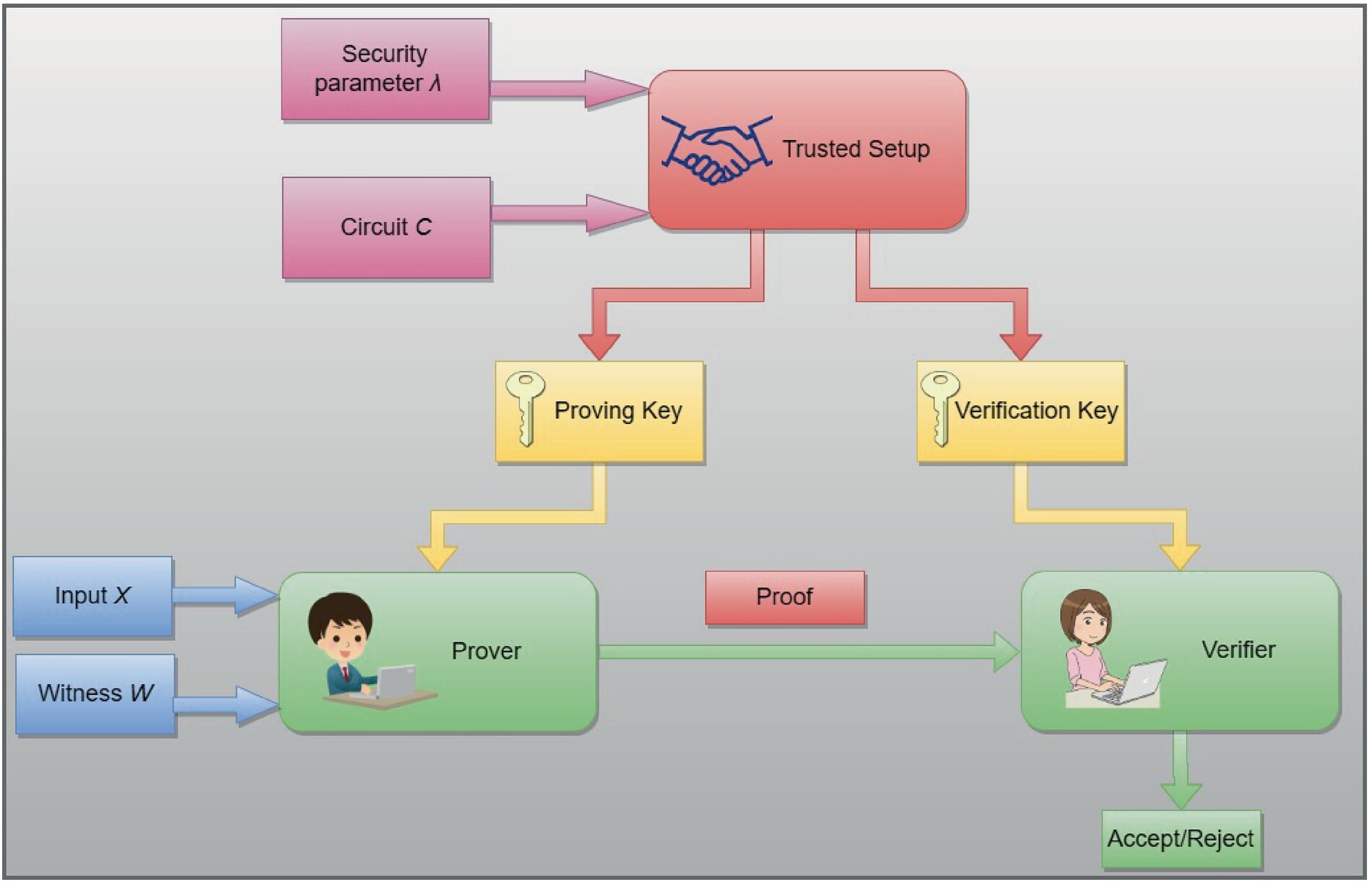

Configuring the zero-knowledge circuit translates your defined predicates into a mathematical structure capable of generating a valid proof. This process bridges the gap between business logic and cryptographic verification, ensuring that the resulting SNARK or STARK proof satisfies regulatory requirements without exposing the underlying user data. The goal is to create a system where compliance is verifiable by third parties while the user’s identity remains private.

1. Define the public and private inputs

The first step is to categorize the data flowing into the circuit. In a zero-knowledge KYC 2026 workflow, you must clearly distinguish between public inputs (verified claims) and private inputs (sensitive credentials).

- Public Inputs: These are the claims the verifier needs to check, such as

is_over_18,is_not_sanctioned, orjurisdiction_is_valid. These values are often hashed or committed to on-chain. - Private Inputs: These are the raw credentials used to prove the claims, such as a passport number, date of birth, or biometric hash. These never leave the user’s device and are never stored by the verifier.

2. translate predicates to arithmetic limits to account for

Next, convert the logical predicates defined in your compliance policy into arithmetic constraints that the circuit can evaluate. This involves mapping business rules to finite field operations.

For example, to prove a user is over 18, you do not simply compare dates. Instead, you calculate the age difference in a finite field and assert that the result is greater than zero. This requires careful handling of edge cases, such as leap years or jurisdiction-specific age thresholds, to ensure the circuit rejects invalid proofs while accepting valid ones.

3. Select the proof system (SNARK vs. STARK)

Choose between a SNARK (Succinct Non-interactive Argument of Knowledge) or a STARK (Scalable Transparent Argument of Knowledge) based on your performance and security needs. SNARKs offer smaller proof sizes and faster verification, making them ideal for on-chain applications, but they rely on a trusted setup. STARKs are quantum-resistant and do not require a trusted setup, but they produce larger proofs.

For most zero-knowledge KYC 2026 implementations, SNARKs are preferred for their efficiency in mobile verification and low-latency on-chain checks. However, if long-term security and transparency are paramount, STARKs provide a robust alternative without the complexity of managing trusted setup ceremonies.

4. Compile and generate the proving key

Once the circuit is defined, compile it into a format compatible with your chosen proof system. This step generates the proving key, which allows the user to generate proofs, and the verification key, which allows the verifier to check them.

The proving key is kept secret and used by the user’s device to generate the proof. The verification key is published and used by the compliance officer or smart contract to validate the proof. Ensure that the verification key is immutable and publicly accessible to maintain trust in the system.

5. Integrate with the verifier

Finally, integrate the verification logic into your compliance platform. The verifier receives the proof and the public inputs, then runs the verification algorithm to check if the proof is valid.

If the proof is valid, the verifier can trust that the user meets the KYC requirements without ever seeing their personal data. This integration should be seamless, allowing for real-time verification of compliance claims in both centralized and decentralized environments.

The user initiates the process by presenting their digital identity credentials to the circuit. These credentials are kept private and are used to generate the proof.

The circuit evaluates the user’s private inputs against the defined public predicates, such as age or sanction status, without revealing the underlying data.

Using the proving key, the user’s device generates a succinct proof that demonstrates compliance with the circuit’s constraints.

The proof and public inputs are submitted to the verifier, which checks the proof against the verification key to confirm compliance.

Deploy the on-chain verifier

The final layer of your zero-knowledge KYC 2026 infrastructure is the smart contract or backend service that receives and validates the cryptographic proof. This component acts as the gatekeeper, ensuring that only users who have successfully completed off-chain verification can interact with your platform. Unlike traditional systems that store raw identity data, your verifier only checks the mathematical validity of the proof against predefined regulatory criteria.

1. Define the compliance circuit

Before writing the contract, you must specify exactly which claims the verifier will accept. In a typical zero-knowledge KYC 2026 workflow, the circuit proves statements such as "the user is over 18" or "the user is not on a sanctions list" without revealing their date of birth or government ID number. Define these inputs clearly, as they become the public parameters of your verification logic.

2. Implement the verification logic

Your smart contract (for on-chain deployment) or backend service (for off-chain validation) must include a function to verify the ZK proof. This involves checking that the proof is mathematically sound and that the user's claimed attributes match the required compliance thresholds. For on-chain implementations, ensure you have the necessary gas budget for heavy cryptographic operations, or consider using a Layer 2 solution optimized for zero-knowledge proofs.

3. Enforce access control

Once the proof is valid, the verifier must grant the user a specific permission, such as a non-transferable NFT or a boolean flag in a state variable. This permission token serves as the credential for subsequent actions, such as trading or accessing restricted features. Ensure that this permission is revocable in case the user's compliance status changes due to new regulatory data.

4. Test with edge cases

Thoroughly test your verifier with both valid and invalid proofs. Verify that it rejects malformed proofs and accepts only those generated by your authorized identity providers. Since zero-knowledge KYC 2026 relies on cryptographic trust, any flaw in the verification logic could lead to compliance breaches or security vulnerabilities. Use formal verification tools where possible to ensure the correctness of your smart contract logic.

Audit for Regulatory Defensibility

To satisfy AML and KYC requirements without violating privacy, your system must prove that verification occurred without storing the underlying Personally Identifiable Information (PII). This approach shifts the compliance model from "collect and store" to "prove what is needed," allowing regulators to audit the validity of the proof rather than the raw data itself.

Start by establishing an immutable audit trail. When a user submits a zero-knowledge proof, log the transaction hash, the timestamp, and the verification result. This log serves as your primary evidence during regulatory reviews, demonstrating that the identity claim was validated against trusted sources at a specific point in time. Ensure this log contains no biometric data, passport scans, or address files.

Next, verify the trustworthiness of the Trusted Third Party (TTP) that issued the initial credential. Your audit process must confirm that the TTP is a recognized entity compliant with local regulations. If the TTP loses its license or is flagged for sanctions, your system must be able to revoke access or flag the credential as invalid. This dynamic verification is essential for maintaining ongoing compliance in a decentralized environment.

Finally, conduct a regular privacy impact assessment to ensure no PII leaks through metadata or side channels. Even if the main database is clean, logs or error messages might inadvertently reveal user attributes. Document these checks to demonstrate due diligence. A robust audit trail proves that you are not just hiding data, but actively managing risk while respecting user privacy.

Common questions about zero-knowledge KYC 2026

As zero-knowledge KYC 2026 moves from research papers to production primitives, users and compliance teams encounter specific technical and regulatory questions. The following answers address the most frequent points of confusion regarding privacy-preserving identity verification.

No comments yet. Be the first to share your thoughts!