In an era where every transaction risks exposing your financial footprint, the OffGrid no KYC crypto debit card emerges as a beacon for privacy enthusiasts. This offgrid crypto card lets you load cryptocurrencies and spend them seamlessly at Visa merchants worldwide, all without surrendering personal data. As of January 2026, it integrates with Apple Pay and Google Pay, capping anonymous spending at $4,000 monthly with instant top-ups. For those prioritizing autonomy over compliance theater, OffGrid delivers on its promise of freedom from banking oversight.

![]()

OffGrid’s appeal lies in its unapologetic focus on user sovereignty. Traditional cards demand ID uploads and endless verifications; OffGrid skips that entirely. Drawing from zero-knowledge proofs and advanced cryptography, it verifies transactions without logging identities. This aligns perfectly with the ethos of decentralized finance, echoing Bitcoin’s censorship-resistant roots while bridging crypto to real-world purchases.

Unpacking OffGrid’s Privacy-First Architecture

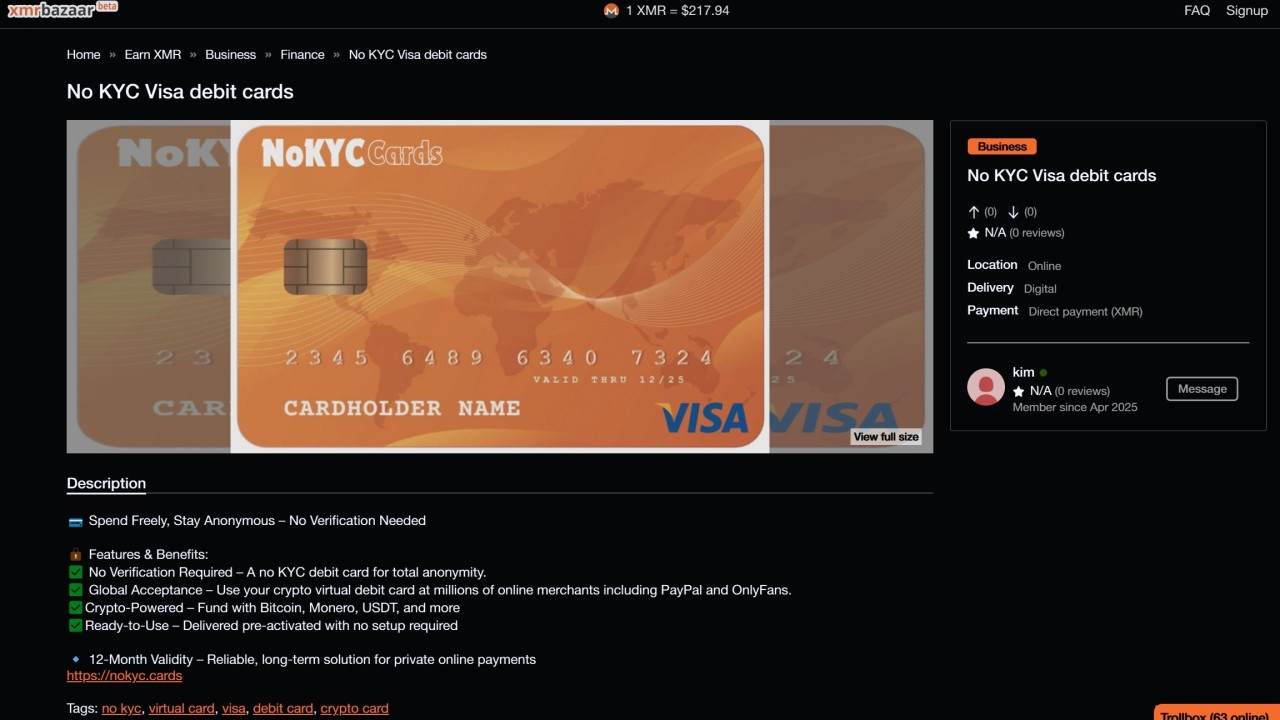

At its core, the no KYC crypto debit card from OffGrid (@offgridcash) rejects the KYC mandates proliferating across crypto services. No passport scans, no address proofs, no questions asked. Users fund the card via compatible wallets, converting assets like Bitcoin or stablecoins on the fly. The platform’s design prioritizes non-custodial control, meaning you retain private keys throughout.

This setup resonates in 2026’s landscape, where no-verification tools dominate niches like anonymous wallets and betting sites. OffGrid extends that to debit functionality, valid anywhere Visa operates. Backed by investors like Draper Associates, who champion no-account privacy plays, it signals institutional confidence in anonymity tech.

Key OffGrid Features

-

No KYC Onboarding: Load and spend crypto without ID verification or personal data collection.

-

$4,000 Monthly Spend Limit: Anonymously spend up to $4,000 per month at Visa merchants.

-

Apple Pay/Google Pay Support: Seamless integration for contactless payments worldwide.

-

Instant Crypto Top-Ups: Quick funding with various cryptocurrencies, no delays.

-

Zero-Knowledge Transaction Proofs: Privacy via advanced cryptography verifying transactions without data exposure.

-

Visa Acceptance Worldwide: Valid at any merchant accepting Visa debit cards globally.

Security merits scrutiny. OffGrid employs end-to-end encryption and multi-signature schemes, mitigating risks common in centralized issuers. While no system is invincible, its non-custodial model reduces counterparty vulnerabilities. Independent audits, though not yet public, would elevate trust; users should monitor for those updates.

Loading Funds: Seamless and Shadowy

Getting started demands minimal friction. Download the app, generate a virtual card, and top up from any non-KYC wallet supporting Monero, Bitcoin, or Ethereum variants. Instant conversions handle volatility, debiting your wallet only upon spend confirmation. Limits start conservatively at $4,000 monthly to balance usability with regulatory evasion, scalable via usage patterns.

For high-privacy seekers, pairing with mixers or privacy coins amplifies anonymity. OffGrid’s cryptography ensures the card issuer gleans no origin data, a step beyond basic mixers. In practice, this means grocery runs or online shops without traceability, a rarity amid tightening global regs.

Spending Limits and Real-World Viability

The $4,000 cap suits daily drivers, covering essentials without drawing flags. Compare to KYC-laden rivals charging fees; OffGrid boasts zero annual or spending costs, echoing top 2026 crypto card lists. Apple Pay integration shines for contactless taps, while Google Pay broadens Android access.

Merchant acceptance spans millions via Visa, from coffee shops to e-commerce giants. Caveat: jurisdictional variances apply. U. S. users might face scrutiny under emerging rules, though OffGrid’s offshore leanings provide buffers. Always cross-check local laws; privacy thrives within bounds.

Real-world testing reveals OffGrid’s edge in everyday anonymity. Users report seamless taps at supermarkets and fuel stations, with conversions executing in seconds. The absence of fees keeps costs predictable, unlike legacy cards nibbling at margins through spreads or inactivity charges. This positions the anonymous crypto card as a viable daily driver for privacy purists chasing spend crypto no id simplicity.

Pros, Cons, and Calculated Trade-offs

OffGrid Card Pros & Cons

-

True zero-KYC onboarding: No ID verification using zero-knowledge proofs for privacy.

-

Instant top-ups from privacy wallets like Best Wallet.

-

$4,000 monthly limit covers essentials for most users.

-

Zero fees: No spending or annual charges.

-

Visa-wide acceptance with Apple Pay & Google Pay.

-

Spend cap limits high-rollers: $4,000/month restriction.

-

Jurisdiction-dependent: Availability varies by local regulations.

-

No public audits yet: Independent verification pending.

These trade-offs reflect deliberate design choices. The cap deters abuse while enabling broad access, a pragmatic nod to sustainability. For heavy spenders, segmenting usage across cards mitigates limits. Absent audits remain a gap; OffGrid could borrow from open-source protocols to build credibility faster. Still, its encrypted crypto card Offgrid mechanics outshine KYC alternatives in data minimization.

Competitor Landscape: OffGrid Stands Apart

In 2026’s crowded field, OffGrid carves a niche among no-KYC peers. Unlike custodial options demanding emails or wallets, it enforces strict non-custody. Rivals in top no KYC crypto credit card roundups often cap at lower limits or tack on conversion fees. OffGrid’s zero-knowledge layer adds forensic resistance, ideal for pairing with Monero mixers.

Backed by Draper Associates’ portfolio ethos of autonomy-first finance, OffGrid anticipates regulatory headwinds. As CBDCs push traceability, Bitcoin-style decentralization via cards like this preserves opt-outs. It complements anonymous wallets and no-ID betting platforms, forming a privacy stack for the vigilant.

Navigating Risks in a Regulated World

No tool evades scrutiny indefinitely. U. S. and EU probes into anonymous spending loom, potentially curbing limits or mandating geo-fences. OffGrid’s offshore structure offers resilience, but users must layer precautions: VPNs for app access, privacy coins for funding, and diversified holdings. Legality hinges on intent; treat it as a compliance tool for lawful privacy, not evasion.

Security incidents remain nil per public records, bolstered by multi-sig and encryption. Yet, phishing targets apps universally; enable 2FA equivalents and shun shared devices. For portfolio managers like myself, integrating OffGrid means allocating 10-20% liquidity to on-ramps, balancing yield farms with spend-ready funds.

Setup unfolds in minutes: install app, link non-KYC wallet, generate card, top up. Virtual-to-physical upgrades arrive post-verified spends. Apple Pay syncs effortlessly, masking crypto origins at point-of-sale. This frictionless flow cements its role in offgrid review 2026 discussions.

Forward-looking, OffGrid eyes expansions like higher tiers for vetted users or NFT collateral. As privacy regs evolve, its cryptography positions it ahead. For CFA-trained eyes scanning trends, this no kyc crypto debit card exemplifies profitable anonymity: spend without surrender, retain control without compromise. Privacy-focused portfolios thrive here, blending seclusion with utility in crypto’s maturing frontier.